A Complete Guidelines Explaining Goods and Services Tax

Goods and Services Tax (GST) has been India's unified indirect tax since 1 July 2017. It replaced the earlier maze of central and state levies and binds the supply of goods and services under one taxation umbrella. This page gives you an overview of GST as it stands today, including the simplified rate structure in force from 22 September 2025.

Introduction to GST

Goods and Services Tax or GST is a destination oriented consumption tax system levied on goods and services supplied in India. The tax is imposed at each stage of manufacture and distribution, and input taxes are set off against output taxes. It is a comprehensive and integrated tax system levied on value addition at each stage.

Get complete assistance required for GST registration

Before July 2017, India had a number of indirect taxation systems through which both state and central governments collected tax, which ultimately imposed double-tax on many goods and services. GST subsumed these indirect taxes and brought stability to India's tax revenue system. The reform has steadily improved tax compliance, in line with the experience of more than 160 countries that use a GST or VAT system.

The Salient Features

Part 1: Dual Model

- Although it is a uniform model for all of India, it has separate components specified for the states and the centre. These are identified as State GST (SGST) and Central GST (CGST).

- These components share the same definition of a taxable event and taxable person, chargeability, measure of levied tax, valuation provisions, the basis of classification etc.

- The SGST is collected by the state government and CGST is collected by the central government.

- This model maintains the constitutional requirement of fiscal federalism for the states and centre as it is defined for federal India.

Part 2: Single Integrated Comprehensive indirect tax:

- Most of the pre-2017 indirect taxes were subsumed under this integrated taxation system called Goods and Services Tax.

-

The central taxes which were subsumed are:

- Central Excise duty

- Service Tax

- Special Additional duties of customs.

- Countervailing duties (CVD)

- Various cesses and surcharges

- In place of these central taxes, CGST is levied on services and goods

-

The state taxes which were subsumed are:

- VAT or Value Added Tax

- Entry tax

- Luxury tax

- Entertainment tax,

- Tax on the lottery, betting, and gambling

- In place of these state taxes, SGST is levied on services and goods. Alcohol for human consumption and five petroleum products (crude oil, petrol, diesel, natural gas and aviation turbine fuel) remain outside GST and continue to attract state VAT/excise.

Registration, Audit, and Documents Required for GST Procedure Get Details

Part 3: Destination based consumption tax

The tax levied on goods and services accrues to the revenue of the place where they are consumed.

For instance, if a seller of Haryana sells a good or service to a buyer in Uttar Pradesh, the tax is credited to the UP government along with the central government.

Getting Registered Under GST

The taxpayers who were earlier enrolled under Central Excise, Customs, Service Tax, VAT and Sales Tax were migrated to GST in 2017. Today, all registrations are made directly under GST.

GST registration is done online through the official GST portal, gst.gov.in. Suppliers of goods with an annual aggregate turnover above Rs. 40 lakh and suppliers of services with turnover above Rs. 20 lakh need to register (the limits are Rs. 20 lakh and Rs. 10 lakh respectively for special category states). Registration is PAN-based: the applicant verifies the PAN, mobile number and e-mail through OTP, completes Aadhaar authentication, and receives a 15-digit GSTIN once the application is approved, normally within about 7 working days.

Documents required to get registered under the GST system are:

-

For the taxpayer:

- PAN of the business or applicant

- Aadhaar of the proprietor / promoters (for authentication)

- Valid personal email address

- Valid mobile number

- Bank account number

- IFSC code

-

Documents required to be uploaded to the website:

- Photograph of promoters / partners / Karta of HUF (JPEG file not exceeding 100 KB in size).

- Proof of business constitution such as partnership deed or business registration certification of the entity (PDF or JPEG file not exceeding 1 MB in size).

- Proof of appointment of authorized signatory (PDF or JPEG file not exceeding 1 MB in size).

- Photograph of authorized signatory (JPEG file not exceeding 100 KB in size).

- The front page of bank passbook / statement which contains the details including bank account number, branch address, account holder’s address and few current transactions.

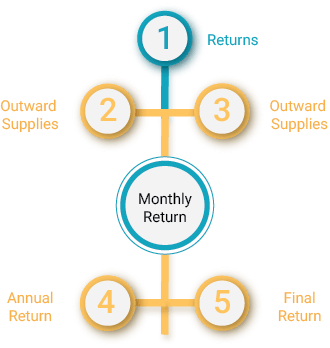

Filing GST Return

Types of GST Return:-

- Outward: GSTR-1, the statement of outward supplies, needs to be filed by the 11th of the succeeding month by every registered person except composition taxpayers, Input Service Distributors (ISD) and TDS/TCS deductors. Quarterly filers under the QRMP scheme can use the Invoice Furnishing Facility (IFF).

- Summary: GSTR-3B, the self-assessed summary return through which tax is paid, needs to be filed by the 20th of the succeeding month (or quarterly, by the 22nd/24th of the month following the quarter, under the QRMP scheme for taxpayers with turnover up to Rs. 5 crore).

-

Other periodic returns:

CMP-08 needs to be filed quarterly by composition taxpayers by the 18th of the month following the quarter, with GSTR-4 filed once a year.

GSTR-5 needs to be filed by non-resident taxable persons for the period of their registration.

GSTR-6 needs to be filed by Input Service Distributors (ISD) by the 13th of the next month.

GSTR-7 needs to be filed by persons deducting Tax Deducted at Source (TDS) under Section 51 by the 10th of the next month, and GSTR-8 by e-commerce operators collecting TCS.

- Annual Return: GSTR-9 needs to be filed annually by 31st December following the end of the financial year (optional for taxpayers with turnover up to Rs. 2 crore; a self-certified reconciliation statement in GSTR-9C applies above Rs. 5 crore).

- Final Return: If any taxpayer or entity decides to cancel the registration, then they need to file a final return in GSTR-10 within 3 months of the date of cancellation or date of cancellation order.

The Advantages of GST for Citizens and for the Economy Get Details

Matching Concept:

Under GST, input tax credit is matched against the invoices reported by suppliers. Both parties need to keep their invoices updated on the portal for the recipient to avail credit.

- First, GSTR-1 is filed by the supplier by the 11th of the succeeding month.

- The invoices reported by the supplier auto-populate the recipient's GSTR-2B, a static input tax credit statement generated on the 14th of each month.

- Input tax credit can be claimed only for invoices appearing in GSTR-2B; mismatches or excess claims have to be reversed and repaid with interest.

- For businesses with turnover above Rs. 5 crore, e-invoicing is mandatory and invoices must be reported to the Invoice Registration Portal to be valid.

Different types of Ledger:

- ITC Ledger of taxpayer continuous

- Cash Ledger of taxpayer continuous

- Tax Ledger of taxpayer continuous

Important Points:

- A registered taxpayer is not allowed to file the GST return for a tax period unless the return for the previous period has been filed.

- A late fee is prescribed for registered taxpayers who file their returns late.

- Late filing of GSTR-1 or GSTR-3B attracts a late fee of INR 50 per day (INR 20 per day for nil returns), subject to turnover-linked caps.

- Late filing of the annual return GSTR-9 attracts a late fee per day of delay, capped at a percentage of turnover, with reduced fees for taxpayers with turnover up to Rs. 20 crore.

- The GST system minimises late filing by providing regular auto-drafted statements (GSTR-2A/2B) for claiming credit and SMS/e-mail reminders before due dates.

Read More About

More about Goods and Services Tax

Applicable GST Rate:

GST began in 2017 with four main slabs of 5%, 12%, 18% and 28%. Under the GST 2.0 rate rationalisation approved by the 56th GST Council meeting and effective from 22 September 2025, the 12% and 28% slabs were abolished: most goods and services now fall under just two main rates of 5% (merit/essential items) and 18% (standard rate), while a 40% rate applies to select sin and luxury goods such as pan masala, tobacco products, aerated drinks, high-end cars, yachts and private aircraft. Special low rates of 3% and 0.25% continue for gold, precious metals and precious stones, and many essentials remain exempt. In brief, taxes are lower for essential goods and higher for luxury and sin goods.

Simultaneous taxation under CGST and SGST for Inter-State transaction:

For the inter-state transaction of goods and services, the tax levied is Integrated Goods and Service Tax (IGST), which is the total of CGST and SGST. It applies when selling goods to a buyer in another state, and IGST is payable after adjusting the available credit of IGST+CGST+SGST paid on buying the goods. The selling state transfers the credit to SGST and the buyer can claim credit for the IGST while discharging SGST liabilities. The centre transfers the credit of IGST used in payment of SGST to the buyer's state. Imports into India are also treated as inter-state supplies and attract IGST in addition to basic customs duty.

Simultaneous taxation under CGST and SGST for Intra-State transaction:

Transactions of goods and services within a state attract SGST and CGST. SGST liability can be paid using SGST (and IGST) credit and CGST liability using CGST (and IGST) credit. No cross adjustment between CGST and SGST credits is allowed.

People Also Searched For